Navigating the UK Convenience

Retail Channel

⏰ 6-7 min.

Why Execution Defines Growth

The UK convenience retail channel occupies a unique and increasingly influential position within the retail ecosystem. Often described as resilient, it has demonstrated a greater ability than many other channels to absorb economic pressure, respond to shifting shopper behaviours and adapt to structural change. Yet resilience alone does not equate to simplicity and for brands success in convenience retail is becoming more complex. As the channel reaches greater maturity, the sources of advantage change. Expansion through footprint, category growth or brand presence are not enough. Instead, performance is shaped by the quality and consistency of execution within the specific operating realities of the channel.

–

A Channel Defined by Frequency, Not Basket Size

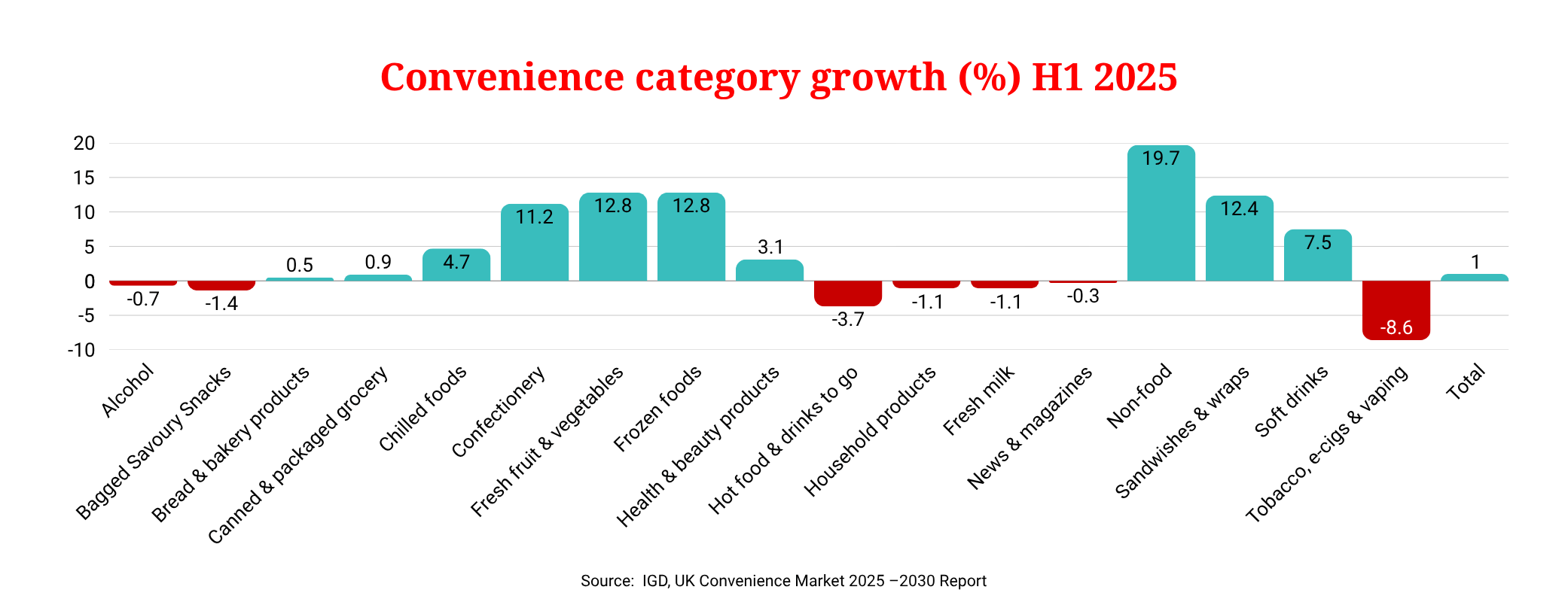

The UK convenience retail market is forecast to reach £56.2bn by 2030, growing at a 2.7% CAGR, slightly behind the wider grocery market, reflecting both resilience and structural maturity In the near term, total convenience sales reached approximately £49.2bn in 2025, with annual growth of around 1.0–1.3%, underlining a low‑growth, high‑competition environment.

Crucially, convenience retail growth is built on frequency rather than basket expansion. Shoppers visit more often but purchase fewer items per trip — shifting the commercial challenge from growing spend per visit to winning a higher share of trips (Lumina Intelligence).

Crucially, convenience retail growth is built on frequency rather than basket expansion. Shoppers visit more often but purchase fewer items per trip — shifting the commercial challenge from growing spend per visit to winning a higher share of trips (Lumina Intelligence).

Unlike traditional grocery, convenience retail is driven by shopper missions, not full‑shop behaviour.

–

–

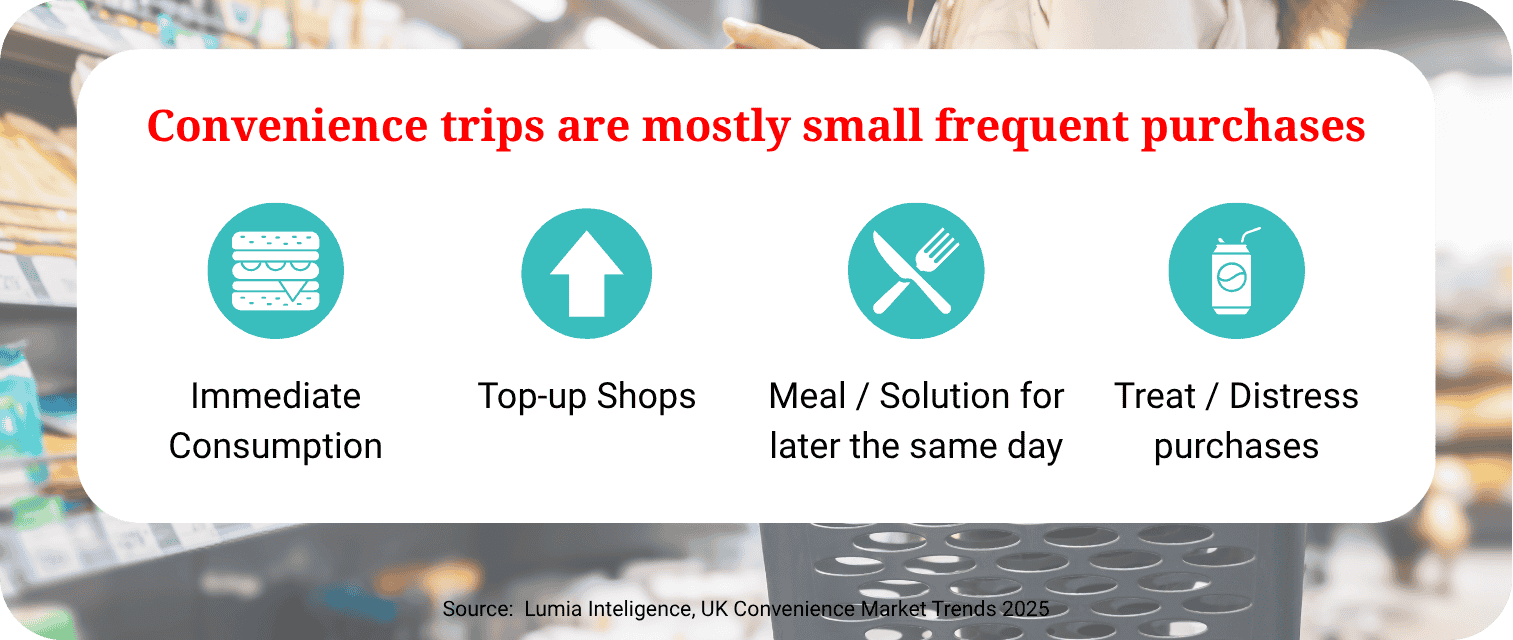

Research shows that convenience trips are dominated by a small number of repeatable missions, including:

- Immediate consumption

- Planned and unplanned top-up shops

- Meal or solution for later the same day

- Treat or distress purchases

These missions cut across all product types: food, drink, grocery, impulse and non‑food. Meaning category relevance alone does not guarantee success. In this context, growth comes from winning a greater share of trips, missions and occasions. Shifting the strategic focus away from range expansion and towards relevance, availability and visibility at the precise moment a decision is made.

–

Availability: The Most Powerful Lever in Convenience Retail

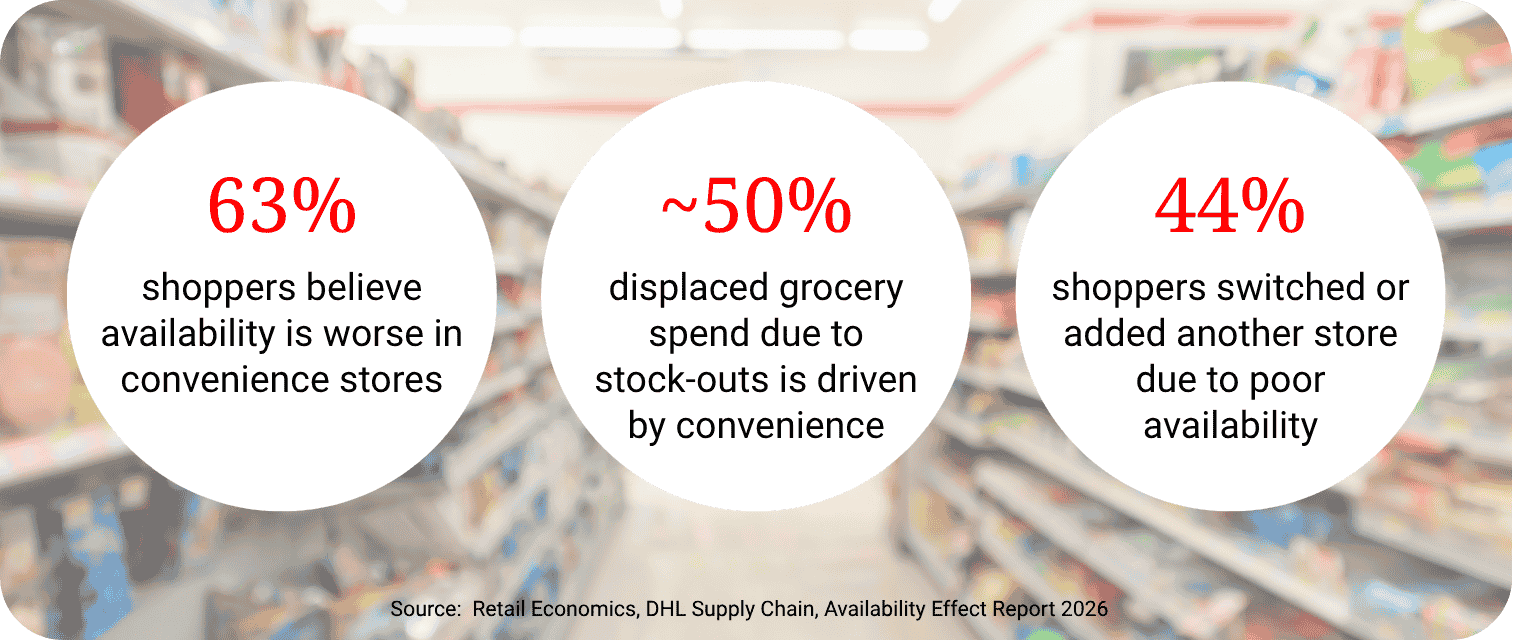

Across all major independent studies, product availability is consistently identified as the strongest driver of sales and loyalty in convenience retail.

- 1 in 5 UK grocery trips involves at least one missing item

- This results in approximately £2.1bn of displaced sales annually

- While convenience stores account for ~20% of grocery trips, they represent nearly 50% of all displaced spend caused by stock‑outs

(Retail Economics, DHL Supply Chain)

–

These figures highlight a structural imbalance. Convenience retail bears a disproportionate share of the commercial cost of poor availability, because tolerance for substitution is lower. Convenience shoppers are typically mission‑led and time‑pressured, for this reason, when a product is unavailable, the sale is redirected to an alternative brand, an alternative store, or abandoned entirely. Availability performance also differs materially by format, reinforcing the challenge for brands operating across convenience retail.

- Typical convenience store availability sits in the low‑to‑mid 80% range

- Supermarkets consistently achieve 90%+ availability

- 63% of shoppers believe availability is worse in convenience stores

(Retail Economics, DHL Supply Chain)

Because the convenience channel is driven by urgency and immediate purchase decisions, availability gaps carry a disproportionate commercial impact. Availability is therefore essential to sustaining brand growth.

While price perception remains a challenge for convenience retail, research shows that price is not the primary driver of loyalty. Around one‑third of UK shoppers prioritise convenience and reliability over price, particularly on time‑critical missions.

–

–

This aligns with broader convenience retail trends, where shoppers are willing to accept a price premium when they trust the store — and the brands within it — to deliver quickly and consistently. In this environment, reliability builds loyalty faster than price investment.

–

One Channel, Multiple Operating Realities

The UK convenience retail landscape is often described as a single channel, but in practice it is a collection of distinct operating models with fundamentally different economics, capabilities and constraints. Growth dynamics vary widely across these models, yet all are bound by the same core execution challenges.

- Multiples convenience are the fastest‑growing segment, driven by scale, investment and consistency

- Symbol groups remain the largest segment but show slower growth

- Unaffiliated independents and many forecourts face greater structural pressure

(ACS)

These differences have important implications for brands. Multiples convenience may offer scale and consistency, but competition for space and visibility is intense. Symbol groups provide reach and local relevance, yet execution quality can vary significantly from store to store. Independents and forecourts often operate with tighter margins and fewer resources, making them particularly sensitive to availability and operational efficiency.

Forecourt‑based convenience stores illustrate this tension clearly. Many are evolving into more destination‑led formats, extending dwell time and expanding food‑to‑go or foodservice offers. However, despite this evolution, their commercial performance remains heavily dependent on foundational retail disciplines — particularly availability, speed and consistency. Enhanced formats do not offset poor execution of the basics. Across all of these models, one principle remains constant: performance is determined locally, store by store. National strategies, listings or promotional plans only translate into growth when they are executed effectively in individual locations. The variance between stores, even within the same fascia or symbol group, often explains the variance in brand performance.

–

What This Means for Brands

For brands pursuing sustainable growth in convenience retail, the evidence points to a consistent set of success factors, regardless of retailer type or operating model. Independent research shows that brands outperform in the convenience channel when they focus on:

- High on‑shelf availability

- Clear relevance to shopper missions

- Strong in‑store visibility

- Execution adapted to retailer type

- Consistency at store level, not just scale nationally

These principles apply regardless of category. What differs is how they must be delivered. Brands that succeed in convenience retail recognise that scale amplifies complexity. Growth depends on the ability to translate national ambition into local performance, aligning availability, relevance and execution with the operational realities of each format. In a channel where success is won or lost in seconds, the brands that outperform are those that treat execution as a core strategic capability.

–

Final Perspective

The UK convenience retail channel will continue to evolve as economic pressure, changing shopper expectations and operational complexity reshape the market. Growth will not disappear, but it will be incremental, uneven and increasingly dependent on execution rather than structural tailwinds. As the channel matures, the sources of competitive advantage narrow.

Macro factors such as footprint expansion, category growth or brand awareness no longer guarantee performance. Instead, outcomes are determined at the point of execution: whether the right product is available, visible and relevant when a time‑pressured shopper makes a decision. In convenience retail, these moments are frequent, fast and unforgiving. This places new demands on brands and national strategies alone are insufficient in a channel where performance is decided store by store, mission by mission. Brands must balance scale with local relevance, and ambition with operational precision.

Availability, reliability and consistency are commercial differentiators. Crucially, success in convenience retail increasingly depends on how well brands align their execution to the operational realities of different store formats, retailer models and shopper missions. The brands that outperform are those that recognise convenience retail as a distinct channel with its own growth logic. Brands that treat execution as a core capability, rather than a downstream activity, are best placed to protect share today and unlock sustainable growth over the long term.

–