Q2 2026 Retail Strategy Guide: Scalable Outsourcing for a ‘K-Shaped’ Economy

Q2 2026 Retail Strategy Guide

Scalable Outsourcing for a ‘K-Shaped’ Economy

⏰ 3-4 min.

As we move into Q2 2026, the European retail landscape—particularly in the UK—is being defined by a “low-volume, high-value” trend. For strategic partners like Acosta Europe, the mission has evolved from providing simple “boots on the ground” to delivering high-velocity, data-driven interventions.

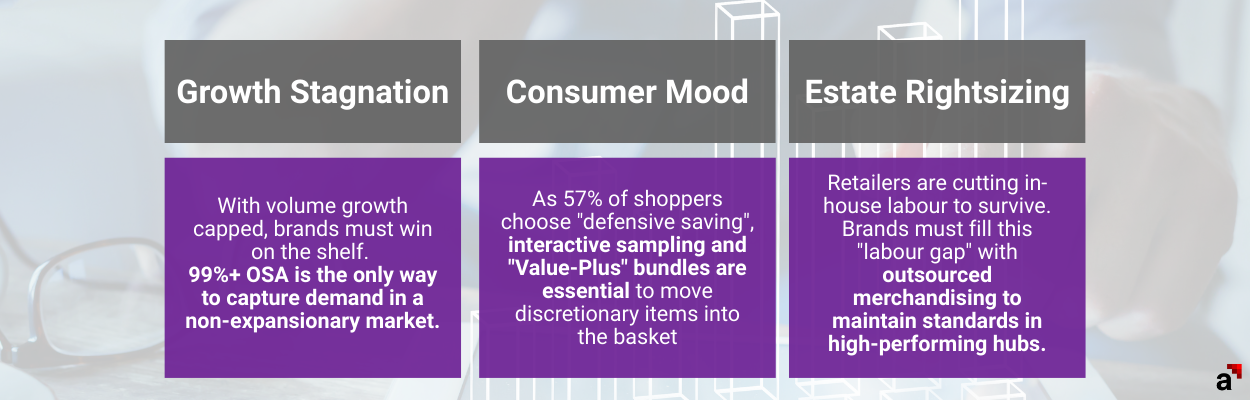

While overall volume growth remains capped at 1.5%, 85% of retail leaders still expect sales growth this year by focusing on operational efficiency and short-term agility.

Sector Performance Forecast

Navigating the K-Shaped Recovery

Consumer spending remains selective. Currently, 72% of consumers are prioritising essentials like food, while 57% are choosing to save rather than spend.

Grocery & FMCG (Strong)

Grocery & FMCG (Strong)

- Q2 volumes are driven by health goals, with fresh fruit (+6%), protein (+9.6%) and fibre-based products (+14.1%) surging as the “ultra-processed” backlash matures.

- With private label at 52.2% share, brands must use Q2 to prove value through nutrient density and availability. If you aren’t on the shelf, the shopper will switch to the store brand.

Health & Wellness (Resilient)

- 40% of consumers now treat wellness as an essential utility. Expect a 13% YoY growth in functional drinks and mood-balancing supplements this quarter.

- Q2 is the window for “Summer Ready” wellness launches. High-impact displays are critical before the Q3 travel surge.

Consumer Tech (Mixed)

- 41% of tech shoppers require a physical demo before buying. However, with 10% of shoppers deferring big-ticket spend, conversion is harder than ever.

- In-store units must be functional and AI-capable. A dead demo unit in Q2 is a guaranteed lost sale.

Fashion & Discretionary (Struggling)

- Still losing 12 stores per day across Great Britain.

- Fashion leads UK e-commerce with 48% digital penetration, making the physical store’s role primarily about brand experience and returns

Macro Threats: The Business Rate “Cliff-Edge”

Macro Threats: The Business Rate “Cliff-Edge”

On 1 April 2026, the UK’s retail tax landscape underwent a structural reset. While the government introduced permanently lower multipliers for smaller high-street units, larger properties now face a property multiplier of 50.8p.

For Retailers

Tier-1 supermarkets and department stores are facing massive overhead spikes. To protect razor-thin margins, many are forced to reduce in-house labour and “right-size” store-level operations, leading to potential gaps in shelf maintenance and customer service.

For Brands

As retailers cut back on staff, the risk of “ghost” out-of-stocks increases. Brands that rely on store staff for replenishment or merchandising will see a decline in On-Shelf Availability (OSA) and a corresponding drop in Q2 sales.

Solution: Investing in Operational Efficiency

Acosta Europe bridges this “labour gap” by transforming fixed operational costs into flexible, high-productivity investments:

Cost-to-Serve Reduction

We take the burden off retailers by providing syndicated and dedicated merchandising teams. By managing shelf-space on behalf of brands, we reduce the retailer’s overhead while ensuring the Brand’s product is always “front and centre”.

Agile Co-Packing & Supply Chain

To counter rising store costs, we offer late-stage customisation and co-packing. This allows brands to bypass traditional warehouse bottlenecks, delivering “retail-ready” displays that require zero in-store assembly.

Data-Led Intervention

We have moved past basic analytics into Agentic AI—autonomous systems that move from “what happened” to “what to do now”. By the end of 2026, it is predicted that 40% of retail interactions will be handled by these agents. Acosta’s field teams use these insights to execute high-value interventions exactly where data shows a margin leak.

Q2 Strategy Summary

Profit in Q2 2026 is won through operational precision. By integrating co-packing agility, experiential conversion, and AI-led field sales, we help brands and retailers absorb cost pressures and capture the “intentional shopper” without increasing fixed headcount.

Profit in Q2 2026 is won through operational precision. By integrating co-packing agility, experiential conversion, and AI-led field sales, we help brands and retailers absorb cost pressures and capture the “intentional shopper” without increasing fixed headcount.